An Expanded Valuation for Commercial Properties – The Gordon Growth Model

Share This Article Today!

The two most common methods used to value an income-producing real estate property are the Gross Rent Multiplier, commonly called GRM, and the Capitalization Rate, commonly called the cap rate.

Both methods are useful, but they measure different things. GRM focuses on gross income. Cap rate focuses on net operating income. The Gordon Growth Model expands the cap rate concept by adding an expected growth assumption to the income stream.

The purpose of this article is to explain GRM, cap rates, and how the Gordon Growth Model can be applied to real estate valuation.

Gross Rent Multiplier

The Gross Rent Multiplier, or GRM, is calculated by dividing the purchase price by the annual gross scheduled income.

| Formula: | Example: |

The GRM method is a simple way to compare income-producing properties because it uses gross scheduled income rather than net income. Gross income is usually easier to identify than net income, and there is less room for expense assumptions to distort the result.

Even if a property is vacant, an investor can often estimate gross scheduled income using market rents. That does not mean the estimate will always be correct, but gross income is usually more straightforward than net operating income.

When comparing similar properties, a lower GRM is generally more attractive, all else being equal.

The downside is that GRM does not account for the costs of owning the property. It ignores operating expenses, maintenance, property taxes, insurance, vacancy, management, reserves, and differences in building condition.

For that reason, GRM can be useful as a quick comparison tool, but it should not be the only valuation method used. For definitions of common real estate finance terms such as LTV, NOI, cap rate, deed of trust, and exit strategy, borrowers, brokers, and investors can also review our Private Lending & Mortgage Glossary.

Capitalization Rate

The capitalization rate, or cap rate, is calculated by dividing the property’s net operating income by the purchase price or market value.

| Formula: | Example: |

Cap rate is one of the most common valuation tools for income property. Investors often search for properties based on a target cap rate. For example, an investor may decide to look only at properties with an advertised cap rate above 8.0%.

However, the advertised cap rate is only as reliable as the underlying income and expense assumptions.

When a prospective property is found, the investor should recreate the operating statement and adjust the income and expenses to reflect the buyer’s likely ownership costs.

Why Adjusted Net Operating Income Matters

Consider the following example:

Example: $1,000,000 Purchase Price

| Seller’s Operating Statement | Adjusted Operating Statement | |

| Gross Income: | $100,000 | $100,000 |

| Property Taxes: | $4,500 Seller’s Tax Amount | $12,500 Estimated at 1.25% of Purchase Price |

| Insurance: | $2,000 | $2,000 |

| Utilities: | $3,500 | $3,500 |

| Maintenance: | $10,000 | $10,000 |

| Vacancy Allowance: | $5,000 Estimated at 5.0% of rents | |

| Reserve: | $2,500 Estimated at $250 per door | |

| Management: | $3,000 | |

| Net Operating Income: | $80,000 | $61,500 |

| Capitalization Rate: | 8.00% | 6.15% |

If the investor’s search criteria required an 8.0% cap rate, this property may appear attractive based on the seller’s operating statement. But after adjusting the operating statement, the actual cap rate may be closer to 6.15%.

This is why investors and lenders should be careful when relying on advertised cap rates.

Buyers and sellers may debate specific adjustments. A buyer may argue that vacancy should be lower, management should be excluded because they plan to self-manage, or reserves should be reduced. Those may be valid points depending on the property and the buyer’s strategy.

However, lenders often underwrite using normalized expenses. A bank or private lender may include vacancy, reserves, management, updated property taxes, insurance, and other operating costs even if the buyer believes their personal expenses will be lower.

That is important because the way a lender views the property may affect the available loan amount, debt service coverage, leverage, and overall financing structure.

Capitalization Rate and the Gordon Growth Model

The Gordon Growth Model is commonly used in finance to estimate the value of an asset based on expected cash flow, required return, and long-term growth.

In financial theory, a perpetuity is a stream of cash flows that continues indefinitely. A basic cap rate valuation is similar to a perpetuity calculation because it assumes the property’s net operating income continues into the future.

However, income-producing real estate often changes over time. Rents may increase, leases may contain annual escalations, expenses may rise, and market conditions may change. Therefore, assuming a 0% growth rate may be too conservative or unrealistic in some situations.

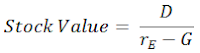

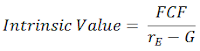

The Gordon Growth Model introduces a growth rate into the valuation.

| Formula Using Dividends: | Formula Using Free Cash Flow: |

|

|

| rE = Required Rate of Return G = Growth Rate D = Dividends |

rE = Required Rate of Return G = Growth Rate FCF = Free Cash Flow |

| Example: | Example: |

The same concept can be applied to income-producing real estate. Instead of dividends or free cash flow from a company, the investor can think about the property’s net operating income and expected long-term growth rate.

Applying the Gordon Growth Model to Real Estate

The key idea is that value increases as expected growth increases, assuming the required rate of return remains the same.

| Metric | 0.0% Growth | 1.0% Growth | 2.0% Growth | 3.0% Growth |

| Net Income: | $100,000 | $100,000 | $100,000 | $100,000 |

| Required Return: | 8.0% | 8.0% | 8.0% | 8.0% |

| Growth Rate: | 0.0% | 1.0% | 2.0% | 3.0% |

| Value: | $1,250,000 | $1,428,571 | $1,666,667 | $2,000,000 |

This table shows how sensitive value can be to the growth assumption.

With $100,000 of net income and an 8.0% required return, the value is $1,250,000 if growth is assumed to be 0.0%. If growth is assumed to be 2.0%, the implied value increases to $1,666,667. If growth is assumed to be 3.0%, the implied value increases to $2,000,000.

The key is determining whether the growth assumption is realistic.

Choosing a Realistic Growth Rate

In commercial real estate, some leases include built-in rent increases. For example, a small retail center with long-term tenants and 3.0% annual rent increases may support a growth assumption above 0.0%.

However, investors should be careful. Contractual rent increases do not automatically mean net operating income will grow at the same rate. Expenses may also rise. Vacancy may occur. Tenants may not renew. Market rents may not support future increases. Capital expenditures may reduce actual cash flow.

For that reason, the growth rate should be supported by the property, leases, market, tenant strength, expense trends, and broader investment assumptions.

A small growth rate may be reasonable in some cases. A high growth rate can create an overly aggressive valuation if it is not supported by facts.

Why Lenders May Not Use This Valuation Method

The Gordon Growth Model can help an investor evaluate long-term value, but lenders may not underwrite a property based on this method.

A lender usually focuses on current value, current income, debt service coverage, loan-to-value ratio, borrower equity, property condition, title, and exit strategy. A bank or private lender may be more conservative than an investor who is underwriting long-term income growth.

This matters because a property may look attractive to an investor using a growth-based valuation but still produce a lower loan amount under a lender’s underwriting standards.

In other words, investor value and lender value may not be the same.

How This Applies to Financing

When evaluating an income property, the valuation method can affect the financing strategy.

A buyer may believe the property is worth more because rents are expected to grow. A lender may base the loan amount on current NOI, current market value, current leases, and conservative expense assumptions.

At FK Capital Fund Inc., we provide business-purpose private lending solutions throughout California, including bridge loans, hard money construction loans, rehab loans, and select real estate-secured financing scenarios. General loan parameters can also be reviewed on our Hard Money Loan Programs page.

For income-producing property, we review the property, borrower equity, valuation support, rent roll, operating income, expense assumptions, lease structure, loan purpose, and exit strategy. Examples of prior lending activity can also be reviewed on our Featured Transactions page.

Final Thought

GRM, cap rate, and the Gordon Growth Model are all useful tools for income property valuation, but each has limitations.

GRM is simple but ignores expenses. Cap rate is more useful because it focuses on net operating income, but it depends heavily on accurate expense assumptions. The Gordon Growth Model adds a growth component, but the valuation can become aggressive if the growth rate is not realistic.

Investors should use these methods as tools, not shortcuts. The right valuation should consider current income, normalized expenses, lease quality, growth assumptions, financing constraints, market conditions, and the investor’s required return.

If you have a California business-purpose real estate financing scenario involving an income-producing property, FK Capital Fund can review the request based on the property, borrower, valuation support, income, structure, and exit strategy.

Submit your loan scenario for review.

For general questions, you can also contact FK Capital Fund here.

Frequently Asked Questions

What is the Gordon Growth Model in real estate valuation?

The Gordon Growth Model can be applied to real estate valuation by estimating property value based on net operating income, a required rate of return, and an expected long-term growth rate.

How is cap rate different from GRM?

GRM uses gross scheduled income and ignores expenses. Cap rate uses net operating income, which makes it more useful for evaluating income-producing property but also more dependent on accurate expense assumptions.

Why does NOI matter in real estate valuation?

NOI, or net operating income, matters because it reflects the income remaining after operating expenses. Cap rate and many lender underwriting decisions rely heavily on NOI.

Can growth assumptions increase real estate value?

Yes. Under the Gordon Growth Model, a higher expected growth rate can increase implied value if the required return stays the same. However, the growth assumption must be realistic and supported by leases, market conditions, and property-level facts.

Do lenders use the Gordon Growth Model to underwrite loans?

Lenders may consider future upside, but they usually underwrite based on current value, current income, debt service coverage, loan-to-value ratio, borrower equity, and exit strategy. A growth-based investor valuation may not support the same loan amount a lender is willing to provide.